How I Manage Money While Traveling

This page contains affiliate links. If you purchase through these links I may earn a small commission at no extra cost to you.

Managing money while traveling can be surprisingly different depending on the country. Some places are almost completely cashless, while in others cash is still essential for everyday life.

Countries like Sweden or China are heavily focused on digital payments, where you can often go days without touching cash at all. On the other hand, countries such as Bolivia or Tajikistan are still very cash-based, especially outside larger cities. Small restaurants, local markets, buses or guesthouses may only accept cash.

Because of this, I usually try to stay flexible and carry a combination of cash and cards.

Cash

Even though cards are becoming more common worldwide, cash is still extremely useful in many countries. In some places it can even save a significant amount of money.

One example is exchanging US Dollars locally instead of withdrawing local currency directly from an ATM. In countries with unstable currencies or multiple exchange rates, bringing USD cash can result in a much better rate. In Bolivia, for example, the difference can sometimes be around 30%, while in Argentina unofficial exchange rates may still offer around 10% more compared to bank rates.

However, exchanging foreign cash is not always straightforward. Many exchange offices only accept large bills such as 50 or 100 USD notes, and they often need to be new, clean and undamaged. Small marks, tears or older series can sometimes be rejected completely or exchanged at a worse rate.

US Dollars are still the world’s number one travel currency and are accepted almost everywhere. Euros are also widely accepted in many countries, although the exchange spread is usually slightly worse compared to USD.

Whenever possible, I also try to exchange the remaining cash from one country into the currency of the next country directly at the border. This does not always give the best rate, but it can be useful to immediately have some local money for transport, food or SIM cards after crossing.

In general, I try to avoid exchanging money too often. Every exchange usually comes with fees or bad rates, so minimizing conversions can save a surprising amount over a longer trip.

Debit and Credit Cards

For long-term travel, I think having multiple cards is essential.

Personally, I believe carrying two Visa cards and two Mastercard cards makes the most sense. Some ATMs only work well with specific card networks, and occasionally certain banks waive fees only for one type of card.

For example, in Japan some 7-Eleven Bank ATMs only allowed free withdrawals with Mastercard, while Visa cards were charged additional fees.

Having multiple cards is also important as a backup. Cards can get blocked unexpectedly while traveling abroad, especially after unusual withdrawals or transactions. Depending on the bank or card provider this can happen more or less frequently.

Before traveling, it is extremely important to check the fees of each card carefully. Many banks charge:

- foreign transaction fees

- currency conversion fees

- ATM withdrawal fees

In addition, many travel cards only include a limited number of free withdrawals per month before additional charges apply. These limits can make a big difference during long trips, especially in countries where cash is used frequently.

Because of this, I try to combine different cards depending on the country and situation instead of relying on a single provider.

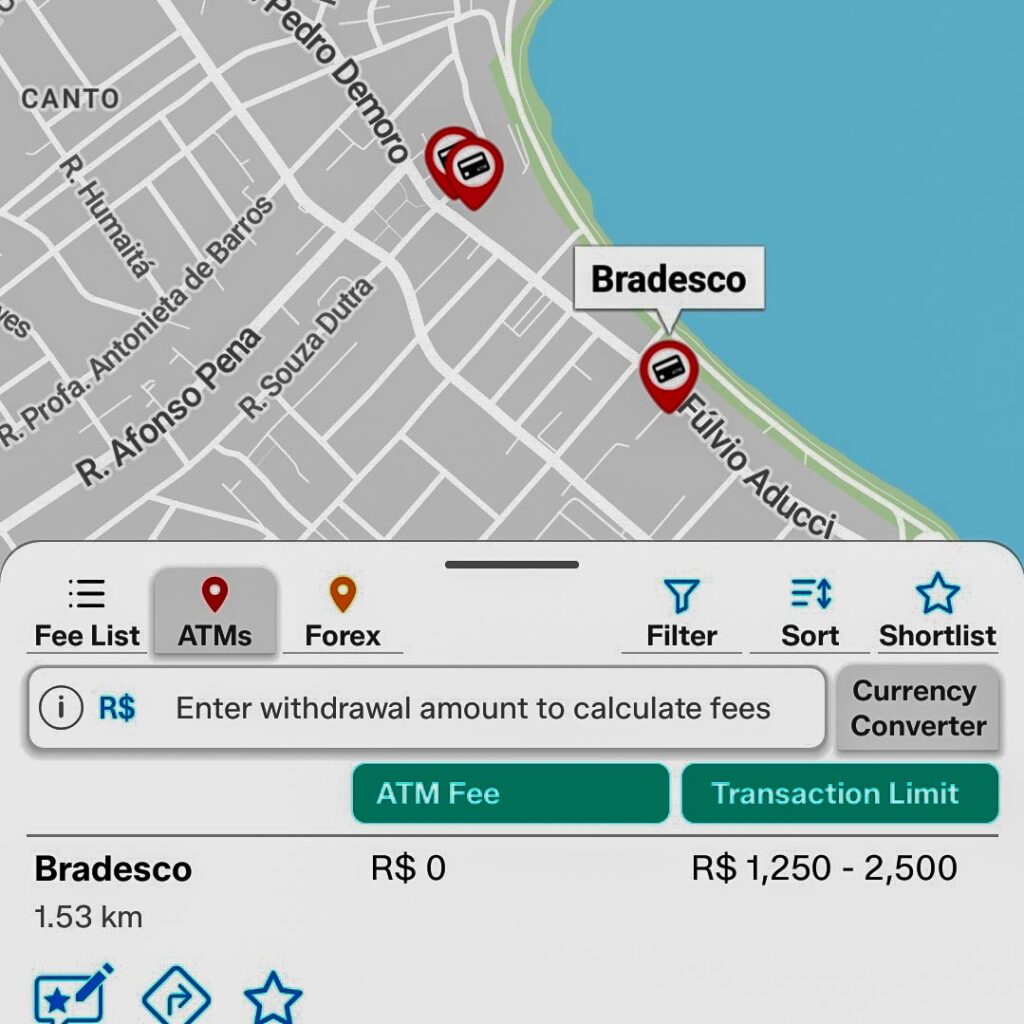

Finding Fee-Free ATMs

To find fee-free ATMs I use the ATM Fee Saver app. It shows fee-free and low-fee ATMs in over 180 countries, including local fees and withdrawal limits.

Important note: The data is not always 100% accurate, but in most cases the ATMs marked as fee-free really are. Not every ATM is listed in the app – once you know which banks usually work without fees in that country, you can search for additional branches on Google Maps.

There is also the official Visa Global ATM Locator, which helps you find Visa/Plus ATMs worldwide (Mastercard has similar locator tools).

This combination of the app, bank knowledge, and card locators has saved me a lot of unnecessary ATM fees.

Staying Connected

For years I have used eSIMs exclusively for local internet access while traveling. A physical SIM might save a few euros in some cases, but the advantages of eSIM are clear enough that I have not looked back.

The practical benefits are straightforward: no time spent searching for a SIM vendor on arrival, no guessing what you are buying in a language you do not speak, and no waiting. You pick a package that fits your needs, activate it before landing, and have a working connection the moment you step off the plane. That last point matters more than it sounds — having internet access immediately at the airport makes finding a taxi or rideshare significantly easier and usually cheaper than whatever is waiting outside arrivals.

The customer service from eSIM providers has also been consistently good in my experience — fast responses, often within minutes, and genuinely helpful when something does not work.

Providers I have used repeatedly with good results:

- MobiMatter (use code Roadsandchains for up to 50% cashback — up to $5 — on your first order)

- GoMoWorld (use code ROADSNCHAINS for 10% discount)

- GlobalYo

QR Payments

QR Payments (QR Code Payments) are a fast, contactless way to pay by simply scanning a QR code with your smartphone. The money is transferred directly from your account or digital wallet—no physical card or cash needed. This technology is spreading rapidly around the world, especially in Asia and emerging markets, because it’s cheap, quick, and easy for merchants to implement. However, for tourists it is often not directly usable. Many systems are tied to local bank accounts, phone numbers, or apps that require a local SIM card, address, or full verification, making them difficult to set up while traveling.

In China, cashless payments have become almost universal. WeChat Pay and Alipay dominate everywhere—from street vendors and taxis to supermarkets and high-speed trains. As a tourist, you can easily link your international credit card (Visa, Mastercard, Amex, etc.) directly in the apps. After a simple verification (usually with your passport), you can scan QR codes or show your own payment code without any hassle. This has made traveling in China much smoother for foreigners in recent years.

Wise now integrates several local QR payment systems directly in the app, making it a great solution for travelers. You can use Alipay+ in countries including the Philippines, Cambodia, Nepal, Sri Lanka, Laos, Maldives, South Korea, Macau, Hong Kong, and Australia.

Get your Wise account here and enjoy low-cost transfers plus convenient local payments on the go.

This combination of global reach and local payment compatibility makes Wise especially useful for digital nomads and frequent travelers who want to avoid high fees and payment friction abroad.

For country-specific tips on getting better exchange rates and avoiding unnecessary fees, see Money Hacks Around the World.